Sansera Engineering Ltd

India's future semi-conductor play?

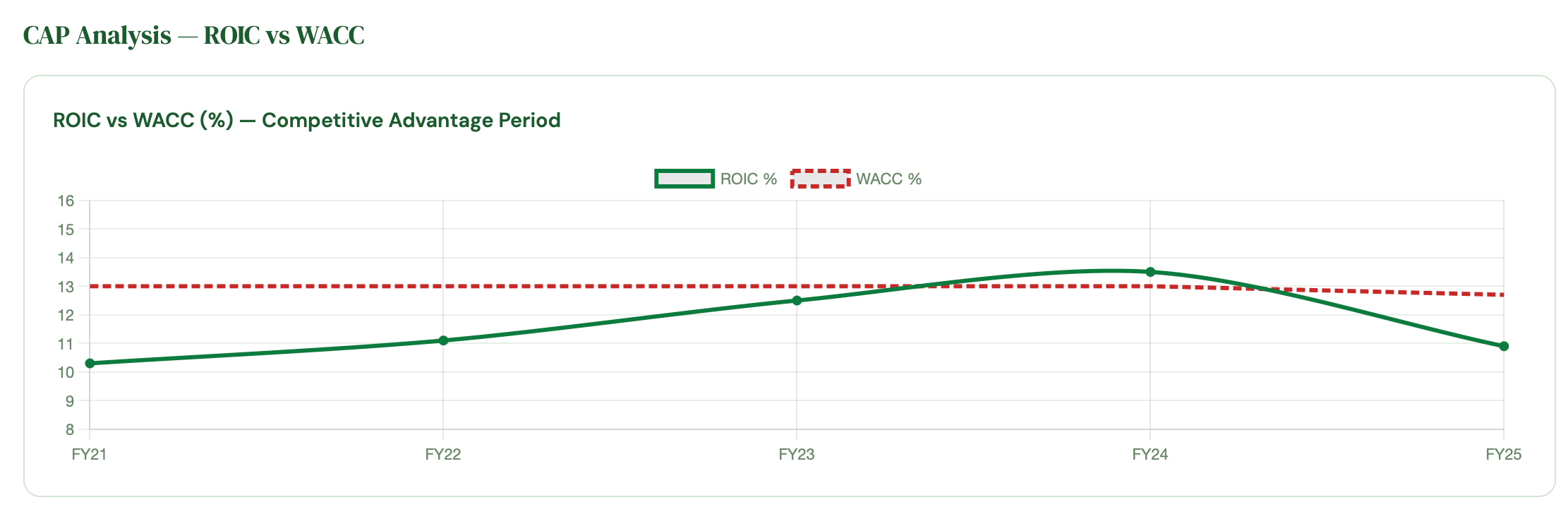

Sansera is undergoing a structural transformation from a predominantly ICE auto-component supplier into a diversified precision engineering platform.

A paid subscriber requested our AI analyst report, I found the transition interesting so sharing with all paid subscribers

every paid subscriber can request 1 report every quarter , become an

The ADS segment is Sansera’s strategic frontier. It serves Boeing, Airbus, ISRO, and a leading global wafer-fabrication equipment manufacturer. The company has received an initial order of USD 17 million from the semiconductor customer, with a ramp target of USD 30 million within three years, and has committed ₹1.2 billion in aerospace machining infrastructure with a second hangar (₹600 crore peak revenue capacity) planned for H2 FY27. The company’s JV with Nichidai (Japan) for broaching tools and its MMRFIC defence-tech investment (₹20 crore revenue, 40% EBITDA margin) further evidence the strategic pivot.

Revenue mix transformation is underway: ICE Auto has declined from 83.4% (FY21) to 71% (9MFY26), while Tech-Agnostic & xEV is at 14% (up from 5% in FY21) and Non-Auto (ADS) is at 15% (up from 12%). The management’s long-term aspiration is to bring non-ICE revenue to 40% — a goal that is structurally achievable but requires sustained order wins and execution over the next 3–4 years.